- Stocks have plenty to focus on in the week ahead, but most important is the fiscal stimulus package making its way through Congress.

- Interest rates have begun to rise again, and for now that is seen as a positive statement on the economy.

- As for the stock market, "I think the path of least resistance has resumed to a higher level. I think we had a mini correction a week ago and I think it happened pretty quickly," said one strategist.

Stocks head into the week ahead with a tailwind, as investors focus on a hefty fiscal stimulus package and the solid earnings season against a backdrop of rising interest rates.

There are several dozen S&P 500 companies reporting earnings, including Coca-Cola, Pepsico, Cisco and The Walt Disney Co. On the data front, there are just a few reports in the coming week, but the consumer price index inflation report is the important one to watch when it is released Wednesday.

Federal Reserve chairman Jerome Powell speaks mid-week at a webinar hosted by the Economic Club of New York.

Stocks surged in the past week, with the S&P 500 jumping 4.65% to a new record high, in its best week since November. The S&P 500 closed Friday at 3,886.

The hyper-activity around short-squeeze names, like GameStop, receded in the past week. Market chatter turned to rising interest rates, the steepening yield curve and market expectations for inflation.

Money Report

"Rates are actually going up as really an expression of the potential that economic activity is likely to start accelerating, and we'll likely see some inflation," said Art Hogan, chief market strategist at National Securities.

Hogan said investors will stay most focused on the $1.9 trillion stimulus package, which Democrats are pushing forward. If it is signed into law at its current size, the total federal spending due to the pandemic would be $5.3 trillion, according to Cowen, an investment bank.

"I think the path of least resistance has resumed to a higher level. I think we had a mini correction a week ago and I think it happened pretty quickly," said Hogan of National Securities.

"I think we continue to grind higher and the only bumps in the road that I can see are a delay in fiscal stimulus or some exogenous factor come in and changes the dynamics," he added.

The market is also depending on continued improvement in new virus cases, said Hogan.

Higher interest rates

The prospect of more spending and an improving economy drove Treasury yields higher in the past week.

The benchmark 10-year Treasury yield was at 1.16% late Friday, after edging to 1.18% earlier in the day, near its recent high of 1.19%.

The 10-year is the most closely watched, as it influences the rates on mortgages and other consumer and business loans. Yields rise as the price of bonds decline.

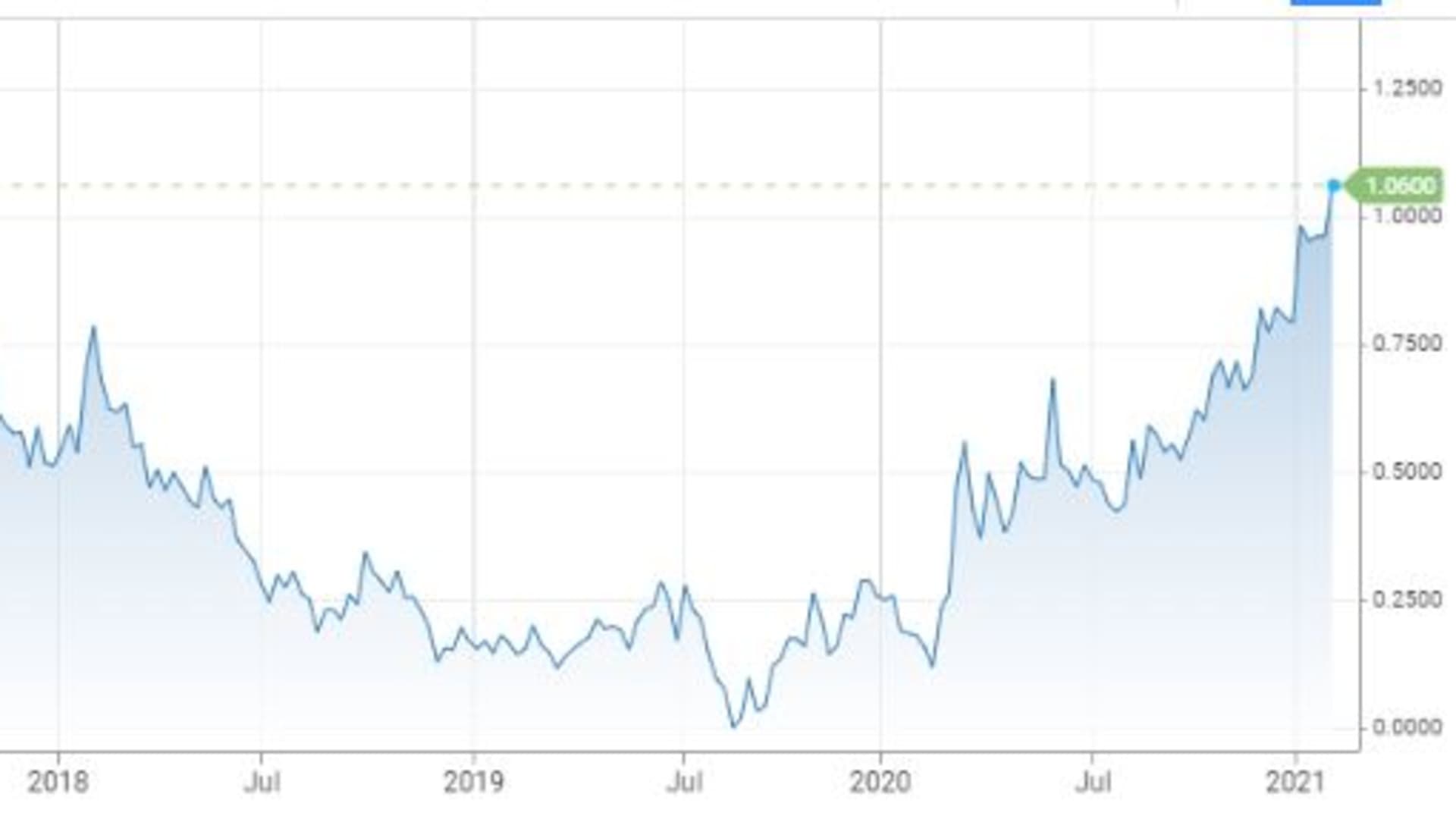

Market pros have also been watching another bond market metric: the yield curve.

It is the spread between the yield on a short-term Treasury, like the 2-year note, and a longer duration Treasury, like the 10-year. In that case, the spread widened to reach 1.06% over the course of the week.

That is the highest level since the second quarter of 2017. A steeper curve — which is what we're seeing today — is viewed as a sign of an improving economy.

Strategists say the move higher in Treasury yields so far is not detrimental to stocks, but instead is a reflection of the economic bounce that could come from the stimulus package.

Tom Lee, head of research at Fundstrat Global Advisors, said the steepening curve is good for the stock market, creating a tailwind for his "epicenter" trade in stocks that will benefit from an improving post-Covid economy.

His preferred sectors are the cyclicals — including industrials, consumer discretionary, materials, energy and financials.

Lee said the selling by hedge funds after short squeezes in a number of stocks and the record decline in the VIX, the volatility index, has led him to change his view on the stock market. He previously expected a sell-off in the first half of the year.

Now, Lee sees a "high probability that the first half 2021 correction is over." The VIX, which is based on puts and calls in the S&P 500, started the week over 33 and fell to 20.87 when the market closed on Friday. A low VIX signals lowered expectations for market volatility.

The sectors that did well in the past week were mostly the ones that will do better in a financial rebound, or in a higher rate environment. Financials were 6.6% higher in the past week as big banks rose along with the yield curve. Higher long-term interest rates are a positive for bank profits.

The industrial group rose 4.9%, and materials were up 3.9%. Energy, lifted by a jump in oil prices, gained 8.3%. Tech recovered some ground, gaining 4.9%.

Sectors that do not do particularly well with rising rates, were up less, including utilities, up 2.3%, and real estate investment trusts, up 3%.

"It's really about having an economic boom, allowing policy to support that boom," said Jim Caron, head of global macro strategies on the global fixed income team at Morgan Stanley Investment Management. "That's the key driver of why the curve is steepening."

Some strategists say the curve is also steepening because of the U.S. will be issuing a lot of debt to pay for the trillions in fiscal stimulus, and that would cause interest rates to rise.

That has also triggered concerns about increasing inflation. While economists do not expect inflation to spike, they do see the potential, for the first time in years, for inflation to move meaningfully above 2%.

Markets will also be monitoring the Senate impeachment trial of President Donald Trump, which begins Feb. 9.

"It will get a lot of attention. Do the markets care? Maybe not, but everyone will be paying attention," said Michael Schumacher, head of rate strategy at Wells Fargo Securities.

Week Ahead Calendar

Monday

Earnings: Hasbro, KKR, Loews Corp., Softbank, Dun and Bradstreet, Take Two Interactive, Nuance, Leggett and Platt, Simon Property Group

12:00 p.m. Cleveland Fed President Loretta Mester

Tuesday

Earnings: Cisco, Twitter, Lyft, Dupont, Mattel, Honda, Nissan, Centene, Hanesbrands, Canopy Growth, Martin Marietta Materials, Masco, Sealed Air, S&P Global, Hains Celestial , Fox Corp, Akamai, Owens-Illinois

6:00 a.m. NFIB small business survey

10:00 a.m. JOLTS

12:00 p.m. St. Louis Fed President James Bullard

Wednesday

Earnings: Coca-Cola, General Motors, Uber, Zillow, Under Armour, Cerner, Zynga, iRobot, MGM Resorts, Spirit Airlines, Lumen Technologies, Molina Healthcare, O'Reilly Automotive, Wyndham Hotels

8:30 a.m. CPI

10:00 a.m. Wholesale trade

2:00 p.m. Fed Chairman Jerome Powell webinar at the Economic Club of New York

2:00 p.m. Federal budget

Thursday

Earnings: PepsiCo, Walt Disney, Kraft Heinz, Expedia, AstraZeneca, Generac, Virtu Financial, Yeti, Kellogg, AllianceBernstein, Borg Warner, Duke Energy, Molson Coors, Tyson Foods, ArcelorMittal

8:30 a.m. Initial jobless claims

Friday

Earnings: Moody's, Newell Brands, ING Groep

10:00 a.m. Consumer sentiment

10:00 a.m. New York Fed President John Williams