- Effective next year, sellers on certain online platforms like Etsy and eBay will receive a 1099-K if their sales are at least $600, down from the current threshold of $20,000 with a minimum of 200 transactions.

- Not all online sales are taxable, whether you receive tax form or not.

- Here's when and how you should be reporting that income to the IRS.

All that money you make selling stuff online? Don't overlook the taxman.

Depending on your situation, it's possible that you're generating income that the IRS wants to know about. And if you're an ongoing seller, be aware that it could become harder after this year to avoid income-reporting requirements.

While the tax law applying to such transactions hasn't changed, it just has become more visible, said Cari Weston, director for tax practice & ethics with the American Institute of CPAs.

Get Southern California news, weather forecasts and entertainment stories to your inbox. Sign up for NBC LA newsletters.

More from Personal Finance:

Buying a Tesla with bitcoin could mean a tax bill

How Social Security benefits are handled at death

A decade-by-decade guide to retirement planning

Under current rules, individuals who sell goods or services via platforms like Uber, Ebay, Etsy and others that use third-party transaction networks (i.e., PayPal) generally only receive a tax form if they engage in at least 200 transactions worth an aggregate $20,000 or more. That form, called a 1099-K, also goes to the IRS.

Starting next year, the federal threshold for issuing the 1099-K will drop to $600 with no minimum transaction level, due to a provision in the recently enacted American Rescue Plan Act. (Some states already have lower minimums.)

This means that in early 2023, you could receive a 1099-K for online sales you make in 2022. And this would be the case whether you're an occasional seller or are operating as a business, as long as you sold more than $600 worth on a single platform. It doesn't necessarily mean you'd be taxed on the money, but you would need to account for it on your tax return.

Ebay is among the platforms that would be affected by the new reporting rule, and the company is working with lawmakers to address any issues it may cause.

Money Report

"EBay believes in following the law and proper tax accounting," said an eBay spokesperson. "Sending confusing 1099-Ks to nearly every occasional or casual seller that uses an online platform to earn extra income, however, is not the right approach."

Additionally, in order to issue a 1099-K, a Social Security number is required, which makes some of the affected companies worry the requirement would be a turnoff to sellers, said Garrett Watson, a senior policy analyst at the Tax Foundation. Not all of these platforms routinely collect that information.

However, because of the current high threshold applied to the 1099-K, even sellers who have a clear profit motive may not receive the form — meaning neither does the IRS, which can lead to underreporting of income.

"A good share of folks on these platforms may not be reporting the income, and the IRS isn't getting that information, either," Watson said.

At last count, the tax gap — the difference between what taxpayers owe and what they pay — was an estimated $381 billion per year, according to a 2019 IRS report that examined data for 2011, 2012 and 2013.

Regardless of whether you receive a tax form, there are instances when the income you earn from your online sales should be reported to the IRS.

Here's what to know about the tax rules that apply.

What's taxable

If your sales are akin to having a garage sale — i.e., you unload belongings for less than what you originally paid — there typically is no reason to report what you pulled in, said Weston at the American Institute of CPAs. Essentially, there is no "income" to report.

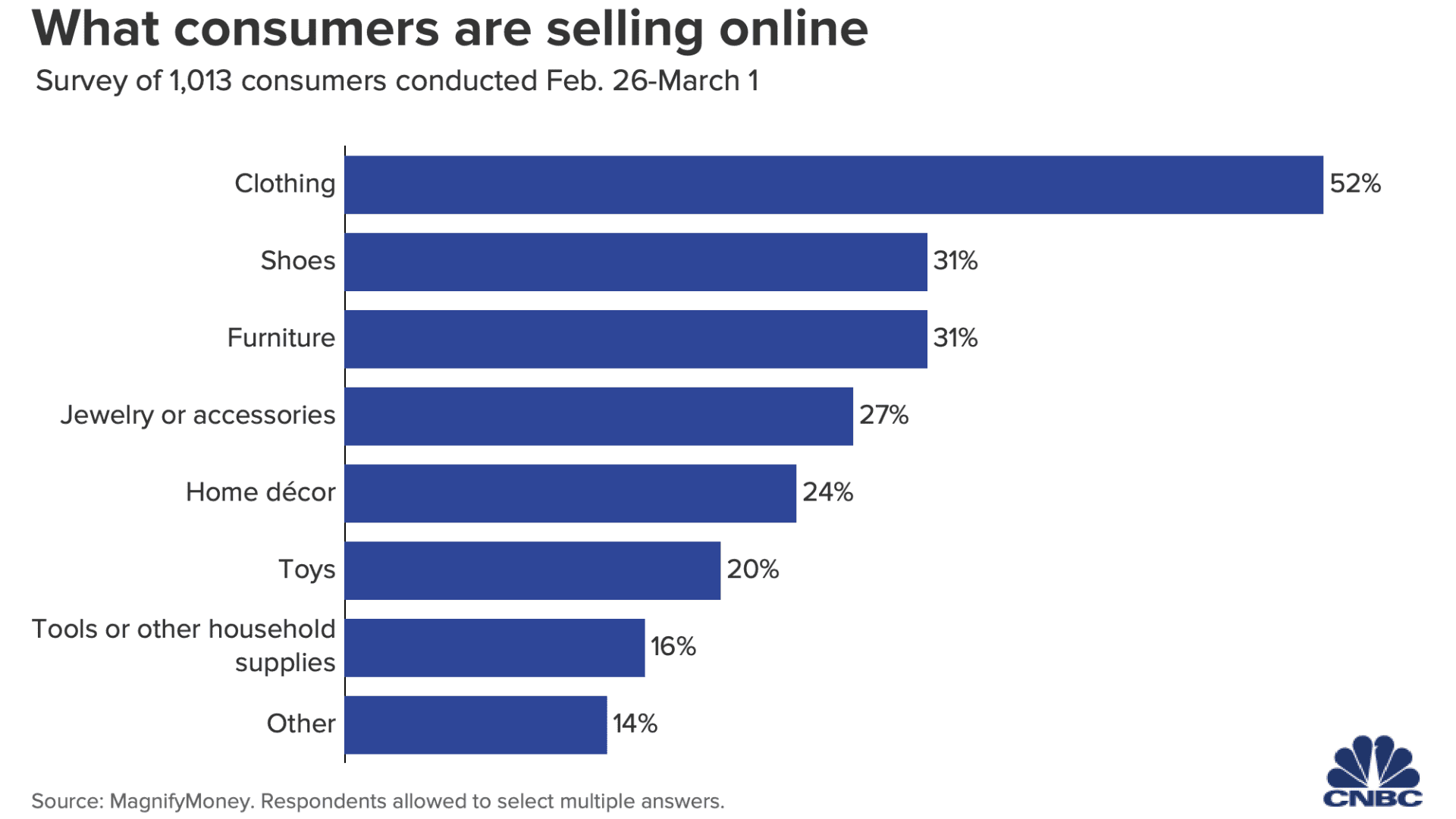

Of those who have sold pre-owned goods on Ebay, for instance, 85% plucked items from their house — things they already owned and no longer used, according to a recent report from Ebay.

Otherwise, the taxation depends on the situation.

Generally speaking, if you're selling to make a profit for reasons that go beyond nurturing a hobby, you probably would be considered a business owner for tax purposes. For instance, if you regularly buy clothes at yard sales (or other discounted spots) and sell them — whether online or not — with the intent of making a profit, that counts.

The good news is that as a business owner, you can subtract your expenses from the money you earn. And if those costs exceed your business income in a particular year, you can subtract the resulting loss from other income you report on your tax return, Weston said.

The IRS expects to hear from anyone whose net earnings from self-employment are $400 or more. And although you would be required to pay self-employment taxes of 15.3%, you can deduct half that amount elsewhere on your return.

The IRS also wants to hear about income you generate from a hobby. Unlike with business losses, though, taxpayers can generally only deduct applicable expenses up to the amount of the hobby income. In other words, the excess (the loss) cannot be deducted from other income.

"However, because it's a hobby and not a business, you don't have to pay self-employment taxes on the income," Weston said.

Figuring out whether you are selling as a hobby or a business can sometimes be tricky. The IRS has some tips on its website intended to help taxpayers make a determination.

Meanwhile, sometimes a belonging is more valuable when you sell it than when you acquired it, whether via a purchase or gift. Your profit generally would be the difference between your cost basis — its value when it came into your possession — and what you sell it for.

In these one-off cases, the profit would get treated as a capital gain. Generally, that means it's either taxed as ordinary income if you held the asset (the item) for less than a year, or else it's considered a long-term gain with a tax rate of 0%, 15% or 20%, depending on your overall income.

However, there are exceptions to those rates, including the 28% that gets applied to gains from the sale of things like fine arts, collectibles, antiques, stamps, coins and some jewelry, Weston said.