- Student loan borrowers have been off the hook from their payments for a year and a half.

- Here are the steps experts recommend borrowers take as their bills come due again.

The other day I did something I haven't done in over a year: I signed into my student loan account. Or, at least that's what I tried to do. Turns out I'd forgotten my password and couldn't get in. Instead of going through the steps to change it, I closed the browser and went back into denial.

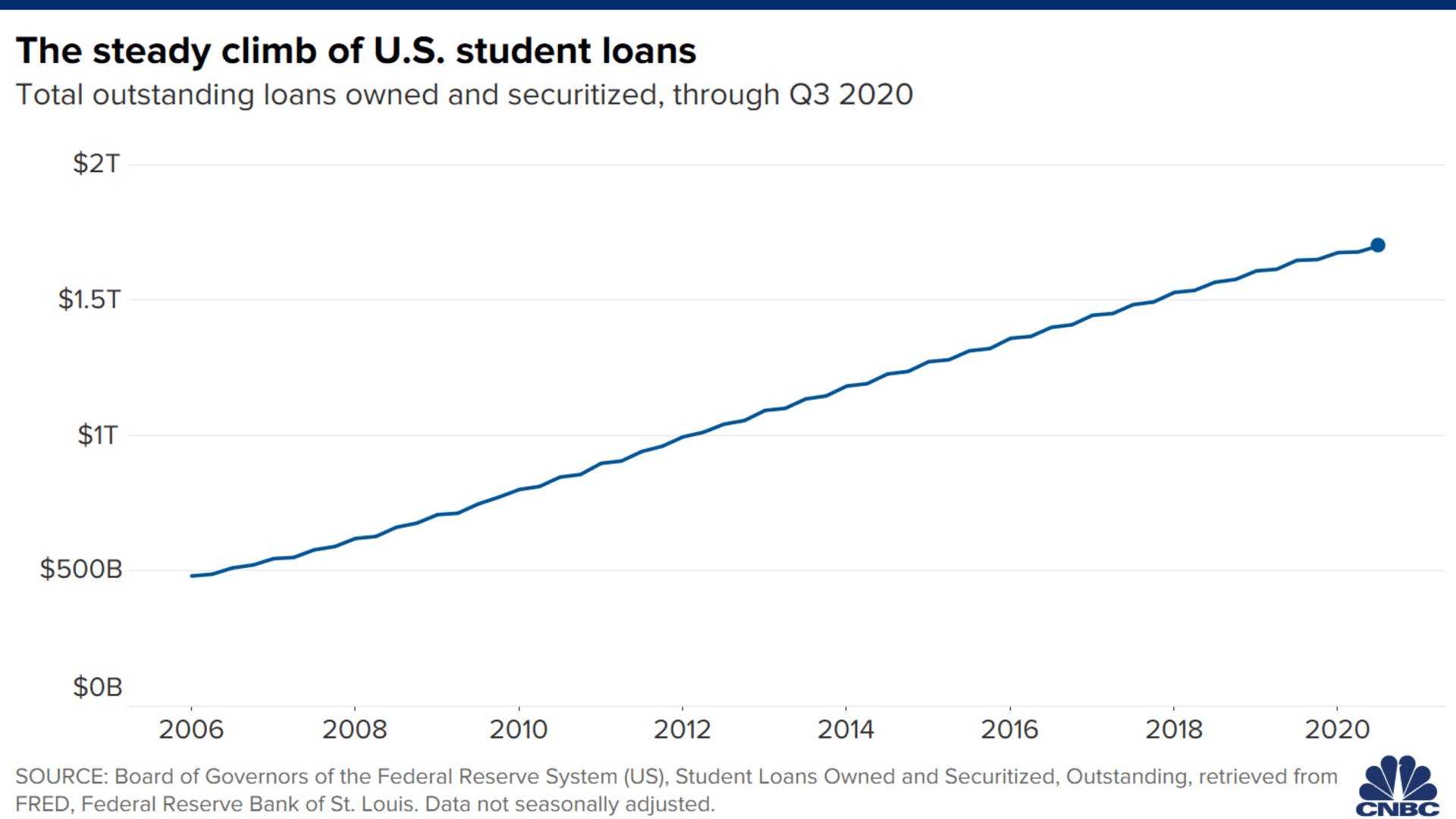

Come this fall, borrowers will again have to make room in their lives and budgets for monthly student loan payments. It's been a good run. The U.S. Department of Education first gave borrowers the option of pausing their bills without interest accruing in March 2020. (Most federal student loan borrowers accepted that offer.)

Many borrowers have grown accustomed to life without a hefty monthly student loan bill, and are likely not looking forward to the break ending in October.

Get Southern California news, weather forecasts and entertainment stories to your inbox. Sign up for NBC LA newsletters.

"Student loan payments have been out of sight, and out of mind," said Elaine Griffin Rubin, senior contributor and communications specialist at Edvisors.

To ease some of your anxiety (and my own!), I spoke to experts about what you need to know about the change and how to best prepare for it.

When will bills be due again?

Money Report

In October. Your exact due date will vary depending on the time of month you began paying your student loans.

There's still a chance borrowers could get more time: Recently, Education Secretary Miguel Cardona said that an extension was under consideration.

"It will likely depend on the state of the economic recovery by then," said higher education expert Mark Kantrowitz. "I doubt they'll extend it beyond the end of the year."

Don't count on getting more time, said Betsy Mayotte, president of The Institute of Student Loan Advisors, a nonprofit.

"While it is still a possibility, it is not guaranteed," she said. "It's best to prepare now — student loan servicer call centers will get busier as we get closer to October."

What should I do now?

Over the next three months, borrowers should make sure that their student loan servicer has their current contact information, Kantrowitz said. If you've moved, for example, they may not.

If you were enrolled in automatic payments and your banking information has changed, you'll also want to notify your servicer of that.

Putting aside some money for when payments begin again may also make the transition less painful, experts say.

What if I'm worried I won't be able to start making the payments again?

If you're still unemployed or dealing with another financial hardship because of the pandemic, you'll have options come October.

First, put in a request for the economic hardship or the unemployment deferment, experts say. Those are the ideal ways to postpone your payments because interest doesn't accrue under them.

If you don't qualify for either, though, you can use a forbearance to continue suspending your bills. But keep in mind that interest will rack up and your balance will be larger (sometimes much larger) when you resume paying.

More from Invest in You:

Suze Orman likes bitcoin. Here's how she says you should invest

How these small businesses pivoted to survive during Covid

Here's how to decide what debt you should tackle first

If you expect your struggles to last awhile, it may make sense to enroll in an income-driven repayment plan. These programs aim to make borrowers' payments more affordable by capping their monthly bills at a percentage of their discretionary income and forgiving any of their remaining debt after 20 years or 25 years.

How do I decide on the right payment plan?

Many people's lives have been changed by the pandemic.

If your circumstances look different than they did more than a year ago, it may make sense to review the payment plans available to you and find one that's the best fit for your current situation.

In the meantime, the law has also changed.

Student loan forgiveness is now tax-free until at least 2025, thanks to a provision included in the $1.9 trillion federal coronavirus stimulus package that President Joe Biden signed into law in March. The policy will likely become permanent.

That may make income-driven repayment plans more appealing, since they often come with lower monthly bills and borrowers will likely no longer be hit with a massive tax bill at the end of their 20 years or 25 years of payments.

But if you can afford it, the standard repayment plan is just 10 years.

To calculate how much your monthly bill would be under different plans, use one of the calculators at Studentaid.gov or Freestudentloanadvice.org, Mayotte said.

If you do decide to change your repayment plan, Mayotte recommends submitting that application to your servicer by the beginning of September.

"I have significant concerns that there will be some big servicing delays," Mayotte said.

Is student loan forgiveness still possible?

Biden has asked the U.S. Department of Justice and the U.S. Department of Education to review his legal authority to forgive student debt through executive action. The fact that those reports are still pending may explain why we haven't heard anything more definitive yet, experts say.

"He's not going to take any steps until that report comes back," Kantrowitz said.

Even if government officials conclude that Biden doesn't have such authority, there could still be hope.

Although Democrats might find it hard to pass legislation forgiving student debt in Congress, given their razor-thin majority, they could turn such a bill into law though the budget reconciliation process in the fall. That avenue wouldn't require the support of Republicans.

Should I think about refinancing my student loans?

Borrowers thinking about refinancing their federal student loans into private loans for a lower interest rate may want to wait, Kantrowitz said. For one, the interest rate on most federal student loans is 0% for at least another three months.

What's more, "they will feel foolish if they refinance only to have the federal government announce loan forgiveness," Kantrowitz said.