Even though the IRS has moved the tax deadline to next month because of the COVID pandemic, the feds are still urging consumers to get their returns filed as soon as possible.

But this season might be more complicated for you this year.

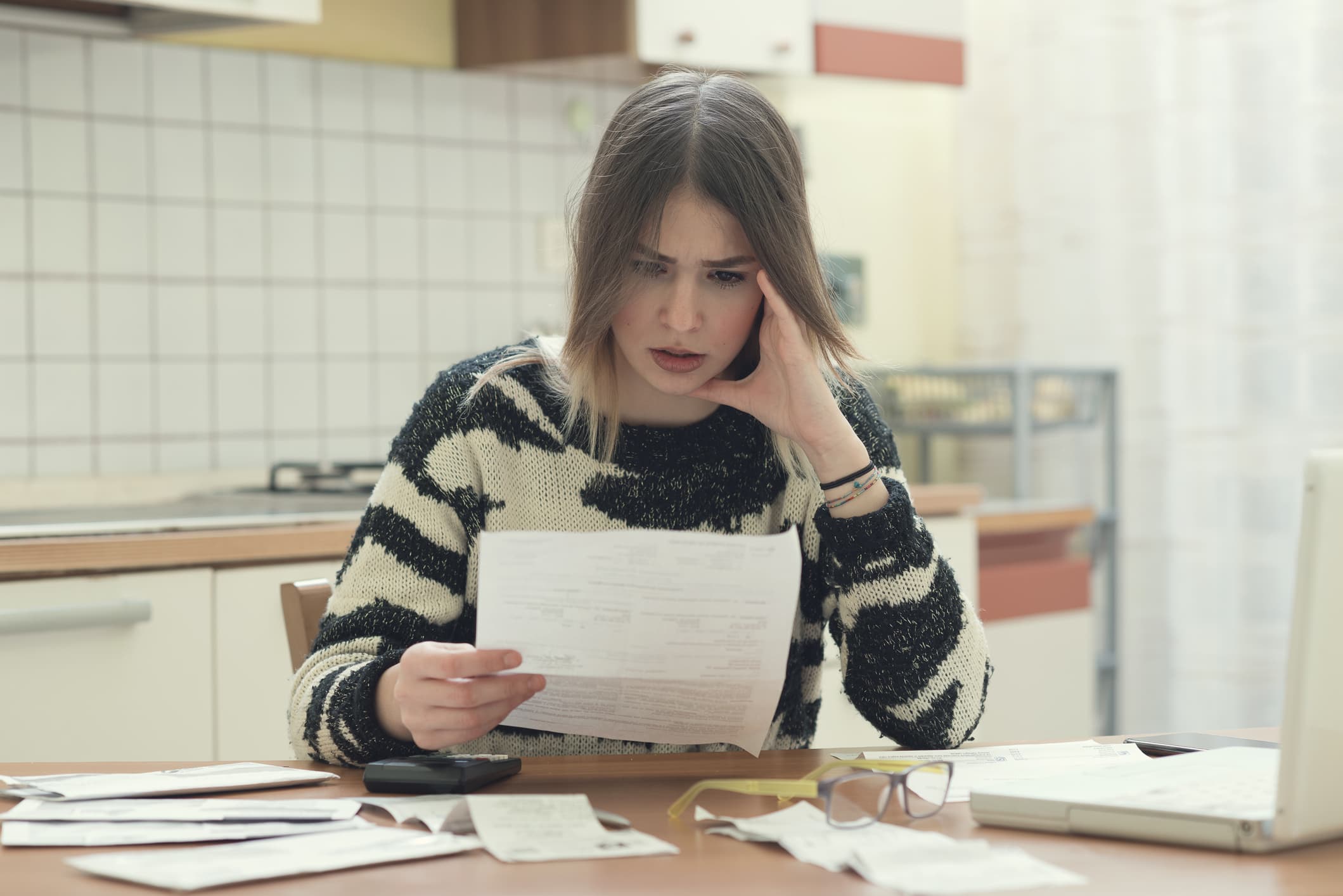

From stimulus checks to unemployment benefits to 401k withdrawals - I-Team consumer investigator Randy Mac breaks down what's taxable and what's not.

Gig worker Crystal Dossett was nervous about tax season. She's never had to pay taxes, so she was not not prepared.

Get Southern California news, weather forecasts and entertainment stories to your inbox. Sign up for NBC LA newsletters.

With her 1099s and stimulus check, Dossett was expecting a tax bill.

"I don't know if I'll have enough expenses to override the income I made to even get anything back," she said.

Dossett isn't the only taxpayer with anxiety, according to Nerdwallet, a personal finance site.

Kimberly Palmer, of Nerdwallet, said tax season is more overwhelming than usual for a lot of people.

According to Palmer, here are some of this year's big issues for taxpayers:

Stimulus checks. Are they taxable income?

- The answer is no. Those checks will not impact your taxes.

What about unemployment benefits?

- "In general with unemployment benefits, you are paying taxes. You certainly are paying federal taxes and the rules by state vary but good news here in California, we don't pay state taxes on those benefits."

Many unemployed workers picked up gig work this year.

If you're one of them, heads up that you'll need to file a Schedule C. It can make filing taxes a little more complicated.

"It basically just means you have to fill in all the different income that you're receiving and make sure you're claiming all of it," Palmer said.

Homeowners who itemize their deductions are allowed to write off their mortgage interest. But if you're in forbearance, you can't. That's because you can only deduct the interest you've actually paid, not accrued.

"The answer is, if you're not paying interest on your mortgage, you can't deduct it on your taxes," Palmer said.

The same is true for student loans. You can only deduct the interest you paid last year. And since the Cares Act temporarily suspended many student loan payments, that means you'll likely only have two months of interest to deduct.

But here's some good news for some current college students.

Nerdwallet says there are multiple deductions available, depending on your income.

Anna Helhoski, of Nerdwallet, said current students and their parents also have a tuition fees deduction of up to $4,000. That will reduce your taxable income if you qualify, she said.

Finally, for those who needed cash last year, the Cares Act also allowed you to withdraw up to $100,000 from your 401k, penalty free.

But - you've still got to pay taxes on that withdrawal, as if it were income. Uncle Sam is giving you time to pay up. You can stretch out the payments over three years.

For those of us now working from home and college students who are schooling from home, unfortunately, there are no deductions for our temporary offices.