- Credit card swipe fees have more than doubled over the last decade, leading some business owners to look for new and creative ways to claw back their profits.

- Main Street businesses across the country are increasingly struggling with changing macroeconomic conditions.

- Visa and Mastercard control 80% of the market, but a proposal in Washington seeks to force greater competition.

Sol Dias Ice Cream, in the Dallas metro area, draws in customers with its award-winning mango sorbet and flavors with a Mexican twist like "tequila" and "queso."

The unique flavors may be what put Sol Dias, with its two locations, on the map, but it's a small placard on the front register that's calling attention.

Get Southern California news, weather forecasts and entertainment stories to your inbox. Sign up for NBC LA newsletters.

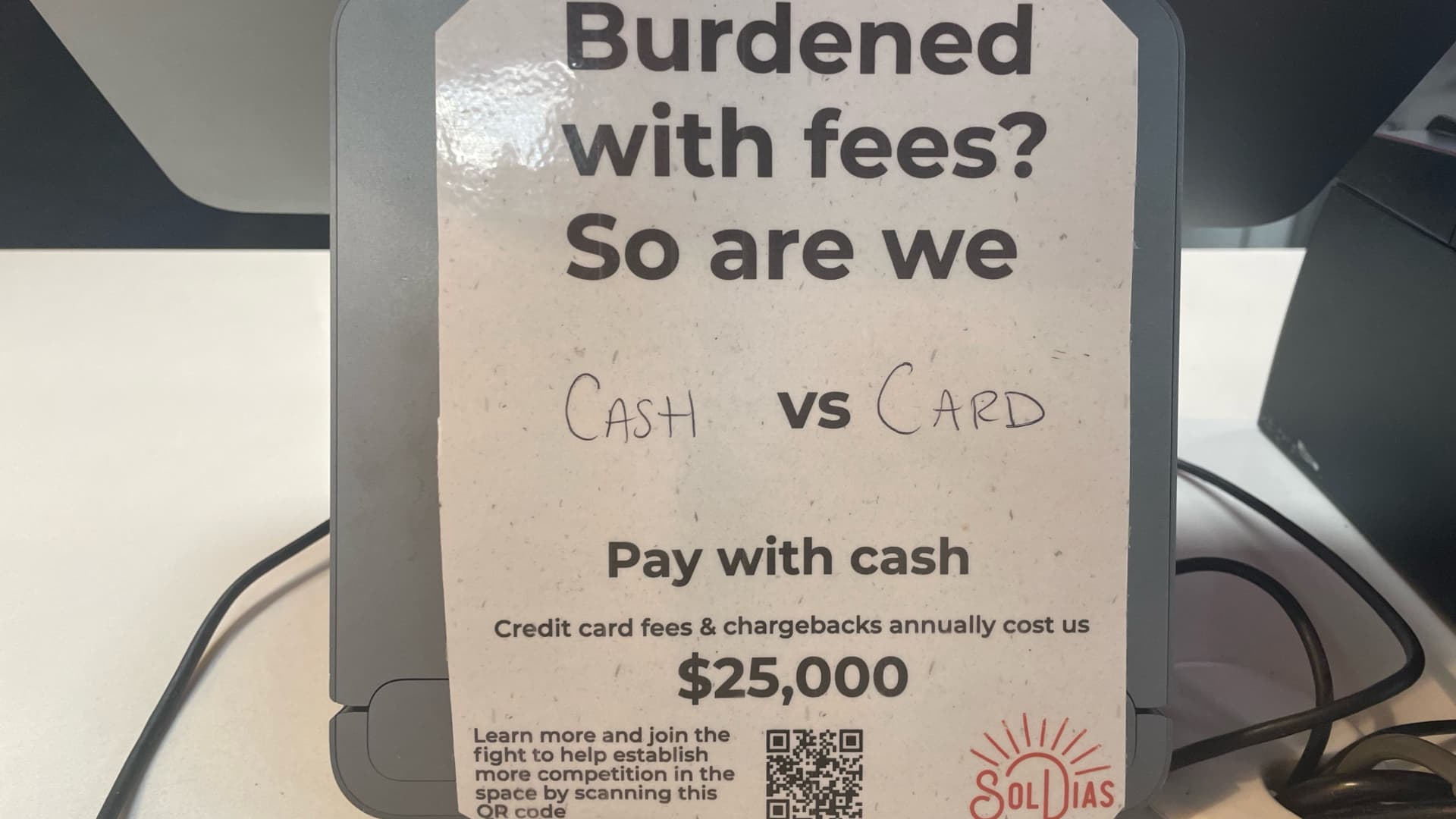

"We have a nice little sign in front of our register that says 'Hey, credit card fees, they cost us a lot of money,'" Victor Garcia, longtime owner of Sol Dias, told CNBC. "Last year they cost us $25,000. This year, they're going to cost us close to $30,000. We're just simply informing the consumer."

Every time a customer pays for their cup or cone with a debit or credit card, companies like Visa or Mastercard charge a processing fee, also known as a swipe fee, amounting to a percentage of each transaction.

The fees have more than doubled over the last decade, leading some business owners to look for new and creative ways to claw back their profits. They're also stirring debate in Washington, pitting payments giants against the small business masses.

The swipe fees aren't new, but the worsening problem comes at a time when Main Street businesses across the country are increasingly struggling with changing macroeconomic conditions. Small business optimism sank to a six-month low in December as owners continued to battle rising costs, according to a survey conducted by The National Federation of Independent Business. That survey found inflation cited as the top concern for business owners.

Money Report

The Federal Reserve's biannual survey of banks' debit card transactions estimates that it costs banks an average of 4 cents to process a transaction, regardless of the total ticket cost. That's down sharply from about 8 cents per transaction a decade earlier. Although the central bank does not conduct the same survey for credit card transactions, the processes used for debit and credit cards are similar.

Meanwhile, credit card fees amount to the third-highest operating expense on average for restaurants, according to the Texas Restaurant Association.

Many small businesses feel they have little choice but to pass on the fees to consumers via higher prices or risk smaller profit margins. Swipe fees drove up prices for the average American by at least $900 in 2021, according to estimates from the Merchants Payments Coalition, which represents a variety of small businesses including restaurants and convenience stores.

Patti Riordan, co-owner of Smoke Stack Hobby Shop in Lancaster, Ohio, said small businesses "lack the volume to be able to negotiate any reduction in fees," which means independent operators pay "the highest prices out there."

Riordan told CNBC she was able to lower her average credit card fee from 2.9% to 1.7% per transaction by switching to a new payments provider — with the help of the National Retail Hobby Stores Association, a trade group for owners like her. Before switching, Riordan said she didn't even know she had the option.

"Those couple of points allowed us to offer health insurance to our full-time people. That's how significant that was," Riordan said.

Swipe fees in the U.S. are among the highest in the world, according to an analysis by payments consulting firm CMSPI. The European Union cracked down on similar increases, capping fees in 2015 at 0.2% for debit card purchases and 0.3% for credit card purchases. In the U.S. the average rate for Visa and Mastercard was 2.22% in 2021, according to market research firm the Nilson Report.

Those higher U.S. fees are partly the result of a higher quality of service, according to Jeff Tassey, chairman of the Electronic Payments Coalition, an industry group that advocates on behalf of payments processors, credit unions and community banks.

"Our systems have much higher value to the consumers. We have the most highly developed consumer credit markets and commerce systems in the world. You get what you pay for," Tassey said.

But Bob Jones, president of regional retailer American Sale, which operates eight pool and outdoor living stores in the Chicago area, said the processors feel less like vendors and more like business partners.

"Their fee is based on a percentage of the sale. So, effectively, they're 2% partners in my business, because that's what they take," Jones said. "Actually, I would say even more because they take the 2% right off the top."

Swipe fees represent the fourth-largest line item for America Sale, Jones said, which is why he's been forced to build the cost into consumer pricing

"There's no getting around it and frankly, there's no getting around it for our competitors," he said.

For many small businesses, step one in combating the fees is customer education. Like Garcia's sign at Sol Dias, which aims to alert diners to the surging fees. A growing number of operators are also looking to credit card surcharges or cash discounts to offset the hikes, according to the Massachusetts Restaurant Association.

Garcia said he wants the right to choose which credit card processing network his ice cream shops use but said he feels "stuck."

Visa and Mastercard control 80% of the market, according to Nilson. Doug Kantor, a member of the Merchants Payments Coalition executive committee, told CNBC that the payments giants set the prices that banks charge, eliminating competition in the space.

"We want there to be more players," said Garcia, whose business is a member of the Merchants Payments Coalition.

The payments giants declined to comment, deferring questions to the Electronic Payments Coalition.

Cash discounts and other incentives did little for Sol Dias to change consumer behavior, which is why Garcia now counts on lawmakers to address the issue.

The Credit Card Competition Act was introduced in both chambers of Congress last year but failed to become law before the end of the congressional session. The legislation would require credit cards issued by the country's largest banks to be processed through at least two different networks.

With more than one route for processing, networks would have to compete over fees, security and service, potentially saving merchants and their customers an estimated $11 billion a year — without affecting credit card reward points — according to an analysis by CMSPI.

The Electronic Payments Coalition, though, claims the bill would affect credit card reward points, and would raise costs for consumers.

"The falsely named Credit Card Competition Act of 2022 was deeply unpopular legislation—among both Democrats and Republicans. This legislation would have hurt consumers through higher costs, weakened payment security, harmed small financial institutions, reduced access to credit for those who need it the most, and ended popular credit card rewards programs," the organization said in a statement.

Sen. Dick Durbin's office told CNBC the Illinois Democrat plans to reintroduce the bill "early this year."